Chapter 4

Count, Track and Reconcile

In his book, Accounting for Fixed Assets, Raymond H. Peterson said: “To manage a profitable business, the management must have information regarding the current location, use, state of repair, and usefulness of its productive assets.”

Many organizations will be familiar with, and have proper procedures in place for counting and reconciling movable assets, like inventory. However, when it comes to fixed asset counting and reconciliation, the same companies will often overlook or neglect to implement robust fixed asset management systems.

Fixed assets, such as land, buildings and manufacturing equipment, will generally make up the biggest part of a company’s balance sheet and investments. A sound fixed asset management system is therefore essential to protect and flush out any inaccuracies in accounting for these valuable resources.

The benefits of proper fixed asset accounting and reconciliation are endless, and includes saving money on taxes with accurate depreciation deductions, saving money on accurate insurance premiums, reducing future theft and fraud and reducing the time it takes to evaluate and account for fixed assets.

Fixed Assets Counting Best Practices

When you start with a fixed asset count and reconciliation, the most important aspect is to start with an accurate foundation. To only way to achieve an accurate foundation is by physically counting the assets.

There are two ways that are generally accepted for a physical asset count:

Full asset verification (also known as wall-to-wall asset verification):

This is a complete and systematic count of all fixed assets in the different locations. Essentially, a blueprint of the building or area is needed to cover every corner. This process might not seem feasible or value adding in large businesses and is more suited to smaller organizations. Similarly, an organization with less spare resources will not always be in a position to conduct a full fixed asset count.

However, it might be necessary to conduct a full asset verification if an initial sampling of assets shows up material inconsistencies from what is recorded in the company books.

Pros of a wall-to-wall fixed asset count

Cons of a wall-to-wall fixed asset count

- Highly accurate results

- Easy to identify damaged or unusable assets

- Time-consuming process

- Can be a big drain on resources

Partial asset verification (also known as cyclical asset verification):

With this method, asset managers would verify fixed assets in stages or through sampling. It is particularly useful if an organization has a large number of assets or if the assets themselves are scattered over a large geographical area.

Multiple, partial asset verifications can be conducted in various business departments and at different times of the year, or through statistical sampling. Sampling would conclude that if you found 90% of assets in your sample, there’s a strong possibility that you would find 90% of items across your entire asset index.

Pros of a partial fixed asset count

Cons of a partial fixed asset count

- Significantly cheaper than the full method of counting

- Not as demanding on resources

- Time efficient

- Results are highly subject to inaccuracies

- Easy to miss damage or unusable assets

Options for Fixed Assets Tracking

A company should have a firm policy in place for the asset tracking. A clear guideline lends to consistency which is highly important in business.

How Does Tagging of Fixed Assets Help?

Tagging of fixed assets is one of the oldest methods for keeping track of assets. It is one of the best methods for physical control of the asset. It serves several purposes.

Easy Identification

It allows for easy identification during a physical inventory. Every company should have a mandate for doing a physical count of inventory. Some companies have the practice of doing this once at year end. Others do it twice a year.

In House Theft Preventative

An asset that is clearly tagged makes it less susceptible to in house theft. It also helps to prevent the asset from being switched by employees. The possibility of this happening is all going to depend on the type of fixed asset. Not all fixed assets are large in size or are easily identifiable by their appearances. A good example of this is computers.

Fixed Assets Tagging Methods

Knowing that fixed tagging is a good business practice now leads one to having to make the decision as to which method is going to be the most acceptable for the type of assets and the business. Tagging is one part of the control of the fixed assets as there has to be a tracking system in place to be able to account for these during accounting procedures.

Using Barcode Tracking

Fixed assets need to be tagged using a numerical system. A descriptive system does not work especially when many of the fixed assets are the same. The barcode system is an easier system then trying to develop a numerical system. It is a time saver for data entry. It does require the use of extra equipment which is the bar code creator which is a specialized printer and a scanner.

Pros

Cons

It is a simplified system with the use of affordable equipment

It has to be scanned during physical inventory

Radio Frequency Identification (RFID)

Tagging can be done with this type of system that allows for two options. They are both based on radio frequency technology.

Using Passive RFID Tracking

The tags that are used do not depend on batteries. A high intensity reader is used that emits a low frequency but a strong radio signal to track the asset. Imbedded in the tag is an antenna. When it detects energy from the reader the circuit in the tag reacts. The reaction creates a message that is transmitted back to the reader but in a different frequency.

Using Active RFID Tracking

The big difference here is that with active RF the tags have batteries, which allow the tags to send their identification to readers. The readers are then able to transfer the data from the tags to a gateway. The data identifies the location of the fixed asset.

Pros

Cons

The reader only has to be in close proximity to the fixed asset and can scan it even if the tag isn’t visible.

More expensive than bar coding

Computerized Asset Tracking

This is a more modern method of asset tracking that can encompass a variety of different methods that includes Wireless applications such as Bluetooth, Cellular and Wi-Fi. It is going to include the use of software to complete the tracking system.

Pros

Cons

- Quick and easy to use can transfer data in a number of different ways

- Data can be integrated with accounting software for accounting tracking

- Will require mounting of readers to rely on electrical power

- More expense with hardware costs.

BLE Beacons

BLE is Bluetooth low energy technology. This is technology that became really notable back in 2013. It is used for a variety of different purposes with one of these for its ability to track people which mean it can easily be used to track fixed assets. BLE receivers are able to detect the tagged asset and send the information through the cloud to either a Wi-Fi portal or send it as cellular data.

Account Tracking

The physical tracking of fixed assets is only one part of maintaining control. The count from the physical inventory now has to be implemented into the accounting records.

The accounting rules differ from inventory tracking in that there is no stipulation to reconcile fixed assets record. The only time this would become a legal requirement would be if an audit were required.

A property registrar should be maintained which is the master property file. This is a file that should have a detailed description of the fixed asset. The tag number should be added to this information. It makes easy where there are many assets and information about one of them is needed then the tag number can be used to retrieve the asset information.

For the tagging process to be used for accountability and tracking the asset should be tagged as soon as it arrives at the company. When the tagging system is carried out efficiently and is accounted for properly than what is on the books for the company as their fixed assets and what is on the floor should be an identical match.

Again though there has to be a policy in place so that every level of the company is familiar with the procedure and there are no breaks or inconsistencies in which the tracking system is carried out.

Approaches to fixed asset reconciliation

It is important to reconcile fixed asset records back to the general ledger on a periodic basis and ideally, the reconciliation should be reviewed by an independent person that’s not part of the reconciliation process.

Reconciliations would generally include information on the original cost of the asset, the accumulated depreciation, any additions, disposals or transfers, capitalized expenses and the closing balance.

Many organizations will use Excel spreadsheets to keep records of this information and calculations. Although Excel spreadsheets might be a sufficient solution when a company doesn’t have significant fixed asset balances, or the asset turnover is particularly low, there are several limitations to using Excel when looking at data accuracy and completeness. Spreadsheets also need constant updating and are prone to human error or document “crashes”.

A great deal of time is required to set up a proper fixed asset reconciliation in Excel while minor errors in manual formulas can go unnoticed causing significant miscalculations. It’s also cumbersome to implement changes in depreciation policies and spreadsheets can be difficult to integrate with other fixed asset solutions.

Fixed asset software packages can mitigate these risks while adding some considerable benefits. A lot of the fixed asset processes can be automated, including depreciation calculations, approvals on acquisitions and disposals, and asset tracking. Time is saved on automatic reconciliations to the most up to date fixed asset inventory information and it is also much easier to scale when a business grows rapidly. Management and audit reports can be produced at the click of a button and software packages will also often be easily integratable with complimentary fixed asset software programs.

But perhaps more importantly is that fixed asset management software is much more accurate because the human interaction level is reduced – asset data will not have to be manually re-entered on a frequent basis.

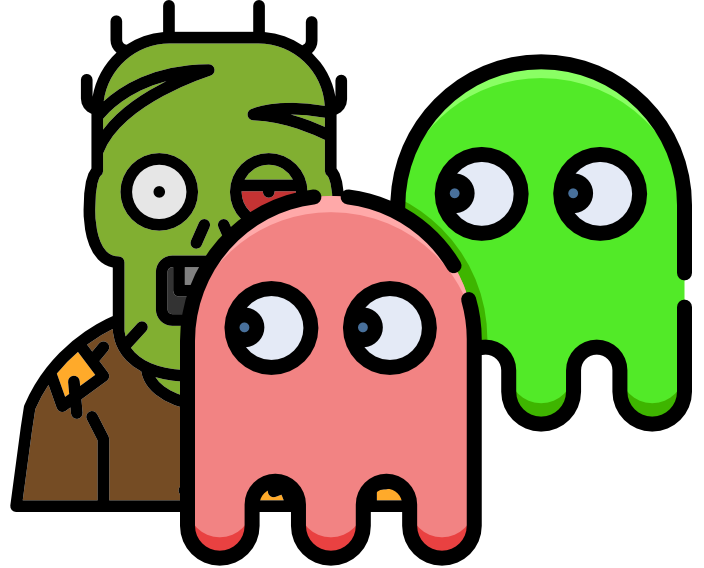

Ghost assets vs Zombie assets: what are they and how they affect your bottom line?

Ghost assets are defined as fixed assets that are unusable, stolen or lost but still accounted for as a fixed asset in a company’s books.

Zombie assets, on the other hand, are capitalized assets that are physically present but not accounted for in any register or in the books.

According to a report by Gartner, up to 30% of all organizations do not know what assets they own, who is using them or where they are located. As much as 70% of organizations have a 30% discrepancy between recorded inventory and actual inventory.

Up to 30% of an IT budget could also be saved by effective asset management, and organizations that implement an effective fixed asset management plan, can reduce the admin cost per asset by as much as 30% during the first five years.

Inaccurate asset ledgers could further result in increased property taxes (often, tax savings of between 20% and 30% are achieved on retiring unused assets).

Ghost assets can cause an unnecessary inflation of insurance premiums while zombie assets that are not insured could have significant cash flow ramifications for a company in case it needs to be replaced when damaged or stolen.

Budgeting for future expansion is also significantly impaired by the presence of ghost and zombie assets. A company might think they possess the necessary assets to embark on expansion plan only to realize the asset does not exist. Conversely, if the company plans for expansion and decide they need to obtain additional resources to do so (land, machinery etc.) but already own these resources, this could result in large, avoidable, expenses.

The importance of accurate fixed asset records when netting out losses and gains

Netting of capital gains and losses on fixed asset disposals can once again afford companies with significant tax savings. It is therefore imperative that assets are recorded and held at the correct values. If there’s been an error in the fixed asset counting or reconciliations, companies stand to lose out thousands of dollars on tax savings.

An example of this would be when depreciation on an asset has been calculated incorrectly, either because the asset has not been recognized for the correct period or it has been under depreciated due to damages that have not been noticed.

This could result in 3 possible scenarios, all leading to a loss of value for the company:

- The asset is sold at a capital gain instead of a loss, resulting not only in a tax liability but also the opportunity cost of not offsetting the loss against other capital gains.

- The asset is sold at an inaccurate, higher accounting gain, resulting in a higher capital gain and therefore a higher tax liability.

The asset is not sold at a high enough gain, resulting in unused capital losses from other assets.

There is a lot of savings potential locked up in improving fixed asset management systems and procedures but unfortunately this is often overlooked by companies.

Inaccurate fixed asset inventory management can cut heavily into increasingly thin operating margins of small businesses and even drastically reduce profits of larger organizations.

The truth is that fixed asset balances will generally make up the lion’s share of any company’s total assets and even the slightest error in its accounting and reconciliation can have a big impact on a company’s bottom line.

Companies can save large sums of money on tax payments, insurance premiums, resource efficiencies, regulatory compliance and a reduction in theft and fraud by implementing a proper fixed asset inventory solution.

Fixed asset management software will further improve best practices and individual asset administration to ultimately optimize the all-important future planning and budgeting phases.